What Happens if You Don't Report Cryptocurrency on Taxes in 2026?

![What Happens If You Don’t Report Crypto on Taxes [US 2026]](https://cdn.buttercms.com/teSc7w2ySjigWbhIGtIz)

Cryptocurrency is taxed in the US. Not reporting crypto on your taxes is a federal offense. The IRS can fine you up to $100,000 and send you to prison for up to five years.

The IRS has made it clear that cryptocurrency is taxable property. Every time you sell, trade, or earn crypto, that's a reportable event. And the agency is no longer guessing who's hiding it.

This guide covers exactly what happens when you don't report crypto taxes, what penalties you face for crypto tax evasion, and how to fix things if you've already missed a filing.

Key takeaways

Cryptocurrency is taxable in the US, and all gains, losses, and crypto income must be reported to the IRS each tax year

Failing to report crypto can result in fines of up to $100,000 and up to five years in prison

If you forgot to report crypto on a past return, you can file an amended return using IRS Form 1040-X within three years of the original filing date

Centralized exchanges like Coinbase, Kraken, and Gemini already report user data to the IRS, and Form 1099-DA reporting is rolling out in 2026

Crypto tax software like Blockstats can calculate your liability and generate IRS-compliant reports in minutes

What happens if you don't report cryptocurrency on your taxes?

Failing to report taxable income from cryptocurrency is considered tax evasion under US federal law.

The IRS treats crypto as property. That means selling Bitcoin, swapping one token for another, spending crypto on goods or services, or earning crypto through staking or mining. All of it is taxable and must be reported.

As of 2026, cryptocurrency exchanges in the United States are required to issue Form 1099-DA to report your capital gains and losses from cryptocurrency.

If you skip reporting, here's what you're actually risking:

-

Civil penalties with fines up to $100,000 (or $500,000 for corporations)

-

Criminal charges that can lead to up to five years in federal prison

-

Back taxes owed plus interest that compounds the longer you wait

The IRS is actively pursuing cases. In 2024, Frank Richard Ahlgren III became the first person sentenced to prison solely for crypto tax evasion. He underreported $4 million in Bitcoin sales and received a two-year federal prison sentence, plus over $1 million in restitution. More recently, Roger Ver, known as Bitcoin Jesus, was arrested on charges that included tax evasion related to Bitcoin holdings and capital gains he allegedly failed to report.

The IRS is watching, and crypto is not a gray area.

Crypto tax evasion and crypto tax avoidance

There's a legal difference between tax avoidance and tax evasion, and it matters.

Tax avoidance is using legal strategies to reduce your tax bill. Things like crypto tax loss harvesting, choosing a favorable cost basis method like FIFO or LIFO, or holding assets longer to qualify for long-term capital gains rates. All of this is legal.

Tax evasion is intentionally hiding income or assets from the IRS. This is a federal crime.

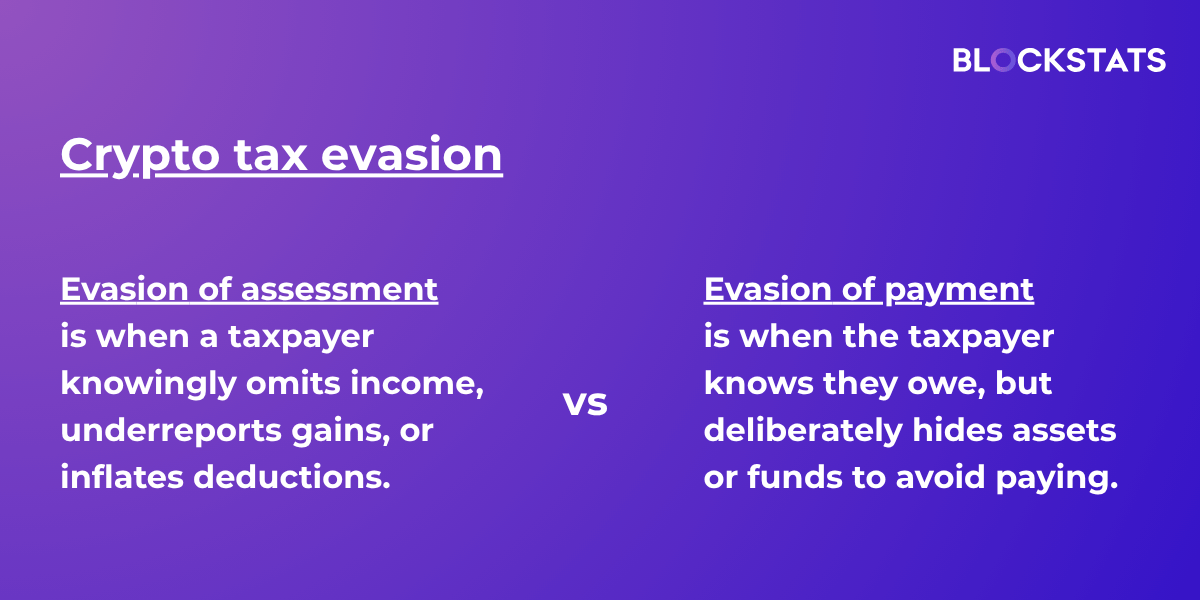

According to the IRS, crypto tax evasion falls into two categories.

Evasion of assessment

This is the more common type. It happens when a taxpayer knowingly omits income, underreports gains, or inflates deductions.

Examples include:

-

Not reporting capital gains from selling or trading crypto

-

Underreporting gains from crypto disposals

-

Failing to report crypto received as income, like staking rewards, airdrops, mining, etc

-

Not reporting business income paid in cryptocurrency

-

Leaving out wages that were paid in crypto

If you sold Bitcoin last year and simply didn't report it, that's evasion of assessment. The IRS considers this willful. And willful is what turns a civil penalty into a criminal one.

Evasion of payment

This happens after a tax assessment has already been made. The taxpayer knows they owe, but deliberately hides assets or funds to avoid paying.

This is less common in the crypto space, but it does happen, especially when someone moves assets across wallets or offshore exchanges to make them harder to trace.

I forgot to report my crypto taxes: What should I do?

If you genuinely forgot or didn't know you were required to report, don't panic.

You have options.

The IRS allows you to amend your tax return up to three years after the original filing date. That means if you missed crypto gains in your 2022 return, you may still be able to file an amendment and correct the record.

The important thing is to act quickly. The IRS is more lenient with taxpayers who voluntarily come forward than with those they catch. Waiting increases the risk of penalties, interest, and, in serious cases, criminal investigation.

If the situation involves a significant amount of unreported income, it's worth speaking with a crypto tax CPA before filing anything. For extreme cases, the IRS Form 14457, the Voluntary Disclosure Practice Preclearance Request, lets taxpayers voluntarily disclose information they previously failed to report, and may help you avoid criminal prosecution if the IRS hasn't already opened an investigation.

How to submit an amended crypto tax return

Forgot to report cryptocurrency on taxes? Mistakes can happen if you've previously avoided crypto taxes, as you weren't aware of your tax obligations.

Amending a crypto tax return is a three-step process.

Step 1: Calculate your tax liability

Before you can file anything, you need to know what you actually owe.

This means going back through your transaction history and calculating:

-

Capital gains and losses: Every time you dispose (sold, swapped, or spent) crypto. You'll need the date of acquisition, cost basis, and proceeds from each transaction.

-

Ordinary income: Any crypto you received from staking, mining, airdrops, or as payment. This is reported at the fair market value in USD on the date you received it.

This is where crypto tax software becomes valuable. Doing this manually across multiple exchanges or wallets is time-consuming and error-prone. A tool like Blockstats can connect directly to your wallets and exchanges, pull your full transaction history, and generate accurate gain/loss reports automatically.

Check out our guide on how to calculate crypto taxes for a step-by-step breakdown.

Step 2: Complete Form 1040X

Once you know your tax liability, download the current version of IRS Form 1040-X, Amended U.S. Individual Income Tax Return.

This form asks you to provide:

-

Your original figures from the previously filed return

-

The corrected figures

-

A brief explanation of what changed and why

You'll also need to reattach any forms you submitted with the original return, like Form 8949 and Schedule D for capital gains, even if those figures haven't changed. If you're not sure which crypto tax forms apply to your situation, our guide breaks down exactly what to file.

Step 3: Mail in or e-file your amended return

Once your Form 1040-X is complete and all supporting documents are attached, you can either mail it to the IRS or e-file it through an approved platform.

If your amendment results in additional tax owed, include that payment with your return to stop interest from accruing further.

After submission, the IRS typically takes 8 to 12 weeks to process an amended return. You can track the status online using the IRS "Where's My Amended Return?" tool.

Can I file my crypto tax amendment with TurboTax?

Yes. If you originally filed through TurboTax, open your previously filed return, and you'll find an option to amend it directly. TurboTax walks you through the 1040-X process and lets you e-file from there. Read our guide on how to file crypto taxes with TurboTax for the full walkthrough.

Penalties for tax evasion

The IRS has a range of penalties depending on whether the issue is negligence, a substantial understatement, or outright fraud.

Here's a quick breakdown:

|

Violation |

Penalty |

|

Failure to file |

5% of unpaid tax per month, up to 25% |

|

Failure to pay |

0.5% of unpaid tax per month |

|

Substantial understatement |

20% of underpayment |

|

Civil fraud |

75% of the underpayment tied to fraud |

|

Criminal tax evasion |

Up to $100,000 fine + up to 5 years in prison |

The civil fraud penalty alone, 75% of the underpayment, can be financially devastating. And if the IRS determines the underreporting was willful, they can refer the case for criminal prosecution on top of civil penalties.

That's why it's always better to file late than not at all.

Will the IRS know if I don't report crypto?

Yes, and the odds of them finding out are growing every year.

The IRS has multiple ways to trace crypto activity:

- Blockchain data: Most blockchains are public ledgers. Every transaction is permanently recorded and accessible. The IRS works with blockchain analytics firms like Chainalysis to match wallet addresses to real identities.

- Exchange reporting: Major US exchanges such as Coinbase, Kraken, Gemini, Crypto.com, Binance US, Robinhood, etc already share user data with the IRS. When you complete a KYC process on any of these platforms, your identity is linked to your transaction history.

- 1099 forms: Many exchanges already issue 1099 forms. Whenever you receive one, the IRS gets a copy too. Form 1099-DA, which specifically covers digital asset transactions, is now being introduced in phases starting in 2026.

- John Doe Summons: The IRS has used this legal tool to compel exchanges like Coinbase, Kraken, and Poloniex to hand over customer data, even when those customers hadn't done anything visibly suspicious.

Assuming the IRS doesn't know is one of the most expensive assumptions a crypto investor can make.

Do all crypto exchanges report to the IRS?

Not all of them — yet. But the ones that matter most already do.

US-based exchanges like Coinbase, Kraken, Gemini, Crypto.com, Binance US, and Robinhood issue 1099 forms to users and share that data with the IRS. With Form 1099-DA rolling out in 2026, reporting requirements are expanding across the board.

Even if an exchange doesn't currently report, that doesn't mean your activity is invisible. Blockchain data is public. And if that exchange ever becomes subject to a summons or regulatory requirement, your historical data could surface.

The safest approach: report everything, regardless of whether your exchange sends you a form.

Read next: How to avoid a crypto tax audit in the USA

How Blockstats tax software can help you file your crypto tax faster

Tracking down transactions across multiple wallets and exchanges, calculating cost basis for hundreds of trades, and making sure everything lands on the right IRS form is a lot. Most people underestimate how complex their crypto tax situation actually is until they're staring at a spreadsheet at midnight before the filing deadline.

Blockstats handles all of it automatically.

Connect your wallets and exchanges. Blockstats supports 500+ platforms, including Coinbase, Kraken, Gemini, MetaMask, Binance US, and Solana. The software pulls your full transaction history in minutes. It calculates your capital gains and losses, identifies taxable income from staking and airdrops, and generates IRS-compliant reports including Form 8949 and Schedule D.

The AI-powered engine also scans for tax-saving opportunities you might have missed, like unrealized losses you can harvest before year-end. It supports DeFi transactions, including complex scenarios like Uniswap LP positions, where most other tools fall short.

When you're ready to file, you can export your reports directly to TurboTax or share them with your accountant.

Stop guessing and start filing with confidence.

Sign up on Blockstats free today and get your crypto taxes done right.

Frequently asked questions

How do I report cryptocurrency on my taxes?

Report capital gains and losses on Form 8949, then carry the totals to Schedule D. Report crypto income from staking, mining, airdrops, or payments on Schedule 1 as ordinary income. Attach everything to your Form 1040. Crypto tax software can generate these forms automatically from your transaction history.

What are the penalties for not reporting crypto?

Civil penalties range from 20% of underpayment for substantial understatements to 75% for fraud. Criminal tax evasion carries fines of up to $100,000 and up to five years in federal prison. Interest accrues on unpaid taxes from the original due date and compounds the longer you wait.

Do you have to report crypto if you don't sell?

Generally, no. Simply buying and holding crypto is not a taxable event. But if you receive crypto as income through staking, mining, an airdrop, or as payment, you must report it at its fair market value on the date received, even if you never sell it.

Do you have to report crypto under $600?

Yes. There is no $600 minimum threshold for crypto reporting. The $600 figure only determines when a payer must issue a 1099 form to you. It doesn't change your legal obligation to report taxable gains or income, no matter how small the amount.

Do I need to report crypto on my taxes if I didn't make a profit?

Yes. You still need to report crypto transactions even if you had a loss. Reporting losses is actually in your favor. Capital losses can offset capital gains and potentially reduce your tax bill. Unreported losses are a missed deduction, not a free pass.

Which crypto exchanges do not report to the IRS?

Most major US-based exchanges already report to the IRS. Some smaller or offshore platforms may not currently issue 1099 forms, but that doesn't make your activity invisible. Blockchain transactions are public, and the IRS can issue summonses to compel data from exchanges. Always report regardless of whether you receive a form.

Will the IRS know if I don't report crypto gains?

Very likely, yes. The IRS uses blockchain analytics tools, exchange-reported data, and 1099 forms to track crypto activity. If you've completed KYC on any major exchange, your identity is already tied to your transaction history. Form 1099-DA reporting, rolling out in 2026, makes this even more comprehensive.

Will I get audited for not reporting crypto in 2026?

Not necessarily, but it raises your risk. The IRS audited roughly 0.6% of personal returns between 2010 and 2018. Unreported crypto income is a known red flag for auditors. Reporting accurately every year is the single best way to avoid a crypto audit risk.